MyFSB NEWS & EVENTS:

A Church Financial Health Seminar Hosted by Farmers State Bank

Church leadership is tasked with more than spiritual leadership, they’re also responsible for stewardship.

At our Church Financial Health Seminar, Farmers State Bank is bringing together local pastors, church administrators, and leadership teams for a free, fast-paced working lunch filled with practical financial strategies, modern tools, and fraud prevention tips tailored specifically for ministries.

This isn’t just another seminar, it’s a chance to gather with fellow leaders, get real answers to pressing questions, and walk away with action steps that protect, strengthen, and grow your ministry.

When: Thursday, July 10th from 11:00 AM - 1:00 PM

Location: Kokopelli Golf Club | 1527 Champions Drive Marion, IL 62959

Doors open at 11:00 AM — come early to check in and enjoy our complimentary taco bar lunch.

Program begins at 11:30 AM with a series of short, high-impact sessions designed to equip and encourage church leaders. Topics include:

-

Fraud & Embezzlement

How to recognize warning signs and protect your church from financial harm. -

Banking Safeguards

Tools and strategies to strengthen your ministry’s financial foundation. -

Insurance for Ministries

Coverage essentials every church should consider. -

Modern Church Marketing

Practical ways to amplify your message and expand your reach.

We’ll close with an open discussion and Q&A to exchange ideas and next steps.

{beginAccordion}

Taylor Shanks of Farmers State Bank Named Finalist for Rising Star in Banking Award

September 12, 2024 – Taylor Shanks, Customer Service Representative at Farmers State Bank, was just recognized as one of the most promising young professionals in banking by The Institute for Extraordinary Banking™.

Taylor was one of three finalists nationwide for the Institute’s Rising Star in Banking™ Award, for demonstrating outstanding leadership, innovation, and dedication.

Charles Holland, CEO of Farmers State Bank, remarked on Taylor’s recognition: “We are incredibly proud of Taylor Shanks for being named a finalist for the Rising Star in Banking™ Award. Taylor’s commitment to excellence, paired with her innovative approach to customer service, exemplifies the values we uphold at Farmers State Bank. Her leadership and dedication to our community have made a significant impact, and this recognition is a testament to the bright future ahead for both Taylor and our bank.”

The Extraordinary Banking™ Awards emphasize the indispensable contribution community banks have on their communities—how deeply woven into the fabric of the community they are. These awards also honor the exceptional individuals within these banks who drive innovation and ensure their institutions continue to serve as pillars of strength and progress.

Community banks are the beacon that illuminates their local communities and the pillar of small business success.

Roxanne Emmerich, Chair and Founder of The Institute for Extraordinary Banking™?, proclaimed during the awards ceremony: “Community banks recognize aspirations, dreams, and silent hopes of small businesses and individuals within their communities. The heart and soul of an extraordinary community bank is the visionary blueprint for the community's success and ability to enact that plan. This year’s Banky awards honor those banks—and the emerging talents within them—who are Top 5 Percenters™ in the industry.”

Farmers State Bank Chooses Autobooks to Elevate Small Business Banking

Expanded digital experience will feature tools built specifically for small and micro-business customers.

April 2, 2024, Marion, IL: Farmers State Bank today announced that it has elected to embed the Autobooks solution for small businesses into their existing digital banking platform. This partnership will enable Farmers State Bank small business customers to get paid online or in-app, directly inside their online and mobile banking.

Autobooks is an emerging leader in digital invoicing and payment acceptance and is a leading integrated-payments provider for small business banking. The integration of the Autobooks invoicing and payment acceptance modules into the Farmers State Bank digital banking platform will help small business owners and nonprofits better manage cash flow and keep track of their customers’ payment status. With just a few clicks, this much-needed tool helps users create and send invoices, schedule recurring invoices, and receive card and ACH payments directly into their Farmers State Bank business checking account.

When asked why he chose to partner with Autobooks, Charles Holland, CEO of Farmers State Bank replied “Autobooks isn't just a partner; they're a source of innovation for small business banking. We've chosen Autobooks to empower our customers because they're not just changing the game – they're rewriting the playbook and ensuring every small business has the tools to thrive, grow, and succeed in today's fast-paced world.”

In addition to invoicing and online payment acceptance, Autobooks offers cash flow management, accounting, and financial reporting tools as part of its full product suite. With Autobooks, Farmers State Bank can deliver workflow-related services that serve their clients’ immediate needs while increasing engagement, loyalty, and profitability.

Autobooks partners with the industry’s leading core processing, digital banking, and merchant processing providers so that Farmers State Bank can quickly deploy to market. This set of integrations, coupled with Autobooks best-in-class go-to-market services, has allowed Farmers State Bank to launch in 15 days and start driving immediate small business adoption.

“Autobooks is the missing piece our small business owners have been searching for,” says Christine Hankins, President of Retail Banking at Farmers State Bank. “With this partnership, we're not just meeting needs; we're exceeding our small business customer’s expectations.”

Legacy Sessions hosted by Farmers State Bank

Thursday, September 14th from 8:00am-1:00pm at the Marion Cultural & Civic Center

The Legacy Sessions, hosted by Farmers State Bank, is a transformative event bringing together renowned experts in the fields of succession planning, estate planning, financial planning, and legacy planning.

During this content-rich event, attendees are immersed in a captivating atmosphere filled with insight, wisdom, and inspiration. Esteemed speakers guide participants on a profound journey of self-reflection, leading them to ponder the significance of their life's work and the impact they can have on their family and future generations.

Through engaging presentations, the Legacy Sessions attendees will explore the details of succession and estate planning and delve into the heartfelt meaning behind creating a meaningful and enduring legacy.

The Legacy Sessions serves as a catalyst for individuals to embrace their responsibility in shaping their legacy, both in their personal lives and in the wider community.

Addressing the Silicon Valley Bank Failure

Farmers State Bank welcomes Cindy Throgmorton as Senior Vice President

November 4, 2022 (Harrisburg, Ill.) – Farmers State Bank announced its Board of Directors has appointed Cindy Throgmorton to be Senior Vice President and Commercial Loan Officer effective immediately. Throgmorton previously held the position of Vice President and Commercial Loan Officer at First Southern Bank.

“We are so excited to welcome Cindy Throgmorton to our Farmers State Bank family,” said Tom Franks, Chairman of the Board. “Cindy brings years of commercial lending experience. With her terrific work ethic and strong Christian faith, she will fit right in with our core values at Farmers State Bank”.

Throgmorton brings a wealth of banking knowledge to her new role as Senior Vice President and Commercial Loan Officer. Throgmorton began her banking career as a part-time teller at Nations Bank in Thomasville, Ga. She is a graduate of CBAI School of Banking and has been a banker for nearly thirty years.

How to Choose a Bank: Farmers State Bank Puts Their Customers First

Farmers State Bank Partner Spotlight with Zogo Finance

Farmers State Bank was recently featured in a case study by Zogo Finance, a financial literacy app for people who want to improve their financial knowledge and get rewarded for learning.

Overview:

Farmers State Bank to Throw Out First Pitch at the Cardinals vs. Reds Game

July 1, 2022 (Harrisburg, Illinois.) – Farmers State Bank of Alto Pass was just invited to throw out the first pitch at the Cardinals vs. Reds baseball game on July 17th, 2022, at 1:15pm in recognition of being named the 2022 Extraordinary Bank of the Year, a national honor for exemplary performance in five areas of banking: philanthropy, customer service, thought leadership, workplace culture, and financial literacy education.

The media is invited to attend and cover the celebratory moment, along with the customers, employees, and Southern Illinois community of Farmers State Bank.

Charles Holland, CEO of Farmers State Bank, is very proud of the many accomplishments that have led to this moment. “Being named the 2022 Extraordinary Bank of the Year is quite the honor for a four – branch, family - owned bank like us,” said Holland. “To throw out the first pitch at a major league baseball game because of what our bank has achieved is just another cherry on top”.

Farmers State Bank is certainly innovative in their pursuit of being an extraordinary bank, especially in how they support their local small businesses and community. During the peak of COVID-19, They successfully processed loan applications from over 1,486 small businesses, amounting to approximately $93 million that will help keep over 3,955 jobs in the Southern Illinois region. In 2022 alone, Farmers State Bank has donated over $80,000 in charitable giving to their area and $25,000 to the Unstoppable Foundation.

Farmers State Bank Named the Top Extraordinary Bank in the Nation | April 2022

April 22, 2022 (Naples, Florida.) – Farmers State Bank of Alto Pass Illinois was just named the top extraordinary bank in the United States by The Institute for Extraordinary Banking™.

Farmers State Bank was singled out as the 2022 Extraordinary Bank of the Year, a national honor for exemplary performance in five areas of banking: philanthropy, customer service, thought leadership, workplace culture, and financial literacy education.

Charles Holland, CEO of Farmers State Bank, believes none of this was possible without the hard work, dedication, and commitment from the people he works with every day. “We reach out to our customers, we give without expectation to our communities, we provide ongoing education for our customers and schools,” said Holland. “We truly believe in our faith and our faith leads us in our decisions and how we interact with our customers, communities, and each other. That is why we are an extraordinary bank”.

The Extraordinary Banking™ Awards highlight the vital yet often overlooked role that local community banks play in our nation’s economy. Without a vibrant local banking industry, our small businesses and families often lack the have-your-back support of a true community bank that makes communities really thrive.

Winning this award also means the Unstoppable Foundation will receive $25,000.00 in Farmers State Banks’ name to build a school in Africa, which is a direct representation of two of their values, philanthropy and financial literacy education.

Roxanne Emmerich, Chair and Founder of The Institute for Extraordinary Banking™, proclaimed during the awards ceremony: “Community banks are the backbone of America. They are what keeps a community thriving. When a community bank leaves a community, small businesses often struggle to stay, and jobs leave. Every robust community has a strong community bank that understands how to help that community thrive and grow.”

Farmers State Bank is looking forward to continuing the momentum of being the best community bank in America. Farmers State Bank leadership, employees, and family members will continue to serve and empower their community in every way they can.

Mike Hopkins appointed Community Bank President and Senior Lender | April 2022

April 29, 2022 (Harrisburg, Ill.) – Farmers State Bank announced its Board of Directors has appointed Mike Hopkins as Community Bank President and Senior Lender effective immediately. Hopkins previously held the position of Senior Vice President of First Southern Bank.

“For me, Mike Hopkins was the obvious choice to be Marion Community Bank President and Senior Lender,” said Tom Franks, Chairman of the Board. “Mike brings years of leadership and lending skills to our team. I’ve known Mike personally for many years and he is a man of very strong faith, the highest moral character, and there is not a finer individual for this position to lead our bank”.

Hopkins brings a wealth of banking knowledge to his new role as Community Bank President and Senior Lender. He began his banking career in 1983 with Banterra Bank in West Frankfort, IL. As of June 1st, 2022, he will begin his 39th year as a banker in Southern Illinois. Hopkins is a proud graduate of John A. Logan College and Southern Illinois University Carbondale with a bachelor’s degree in Marketing.

Farmers State Bank is coming to Herrin in late 2022

March 14, 2022 (Harrisburg, Ill.) – Farmers State Bank of Alto Pass is pleased to announce the development of their fifth branch to be located at 1720 South Park Avenue in Herrin, Illinois. To celebrate the new location, Farmers State Bank recently hosted a community leaders’ dinner, revealing the first renderings of the soon-to-be Herrin branch. The new location is set to break ground later this month.

“We are thrilled to show the fine folks of Herrin what true community banking is all about,” said Tom Franks, Chairman of the Board of Directors. “We plan to plug in to every aspect of the Herrin community including academics, athletics, philanthropy, and wherever else we can serve. We are not here to take; we are here to give”.

Farmers State Bank is already involved in the Herrin community, especially with the schools. Farmers recently sponsored the FBLA Etiquette Dinner and the Senior Breakfast where they introduced students to a financial literacy app enabling them to make informed and effective decisions as they transition into adulthood. Along with being a proud Herrin athletics sponsor, Farmers looks forward to offering academic scholarships starting in 2023. Farmers is a member of the Herrin Chamber of Commerce and an active participant with Herrin Festa Italiana.

Farmers State Bank | EThOs Mastermind Class

What is a Mastermind?

A mastermind is a group of smart people who meet to tackle challenges and problems together. They lean on each other, give advice, share connections and do business with each other when appropriate. The power of the mastermind is not just in the leader but the leaders ability to get the right people in the room to create a community where people feel open to ask questions, challenge ideas and come together.

At Farmers State Bank, we believe in the power of community so deeply that we want to create one: one where you can be vulnerable about where you stand financially, share things that have worked or didn't work for you in the past, and foster an enviornment of learning as a collective. If we can commit to learn together and show up for each other both in support and in knowledge, we can keep the community moving forward as we work towards our financial goals and navigate life together.

The most powerful thing about masterminds is that we all bring something to the table. It's about the quality and caliber of people from all different industries bringing their gifts and experiences to the table - that's the real power.

Farmers State Bank has four mastermind groups throughout the year for you to choose from. Each one is different so it's important that you make sure you choose the one suites you best. All of them are free for you to join.

-

February 17th - April 28th: Smart Women Finish Rich Mastermind (IN SESSION NOW)

- May 12th - July 14th:

- July 28th - September 29th:

- October 13th - December 15th:

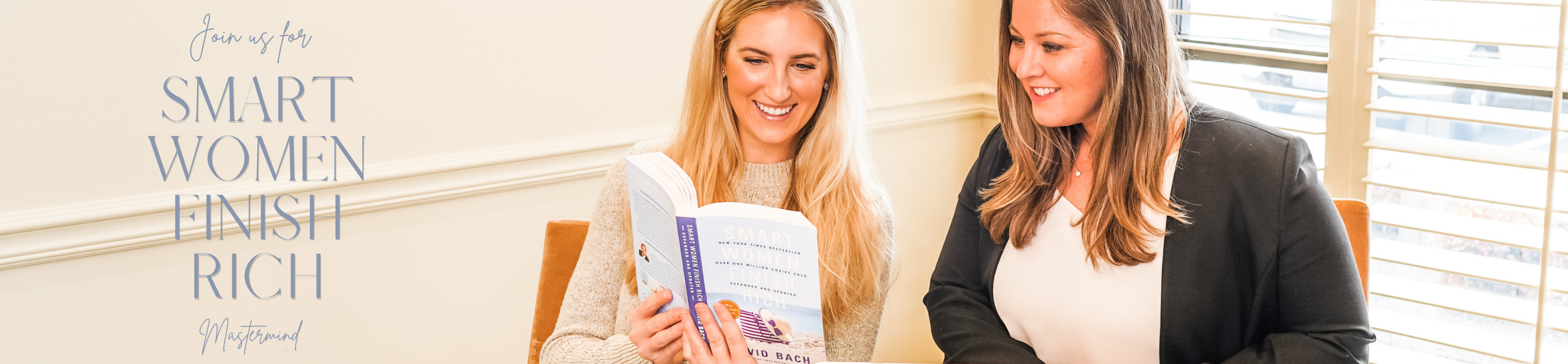

Farmers State Bank | EThOS Smart Women Finish Rich Mastermind

Calling all smart women...

Are you ready to join a community committed to not just helping you reach true financial security, but the power to experience a future of fulfillment and freedom based on your values?

Join our Smart Women Finish Rich Mastermind!

How does it work?

Each Smart Women Finish Rich Mastermind lasts a total of 10 weeks. We will meet from 12:00-1:00 pm each Thursday afternoon at EThOS at the Citadel Building on the Square in Marion where we will come together as a whole, talk about what we learned while reading Smart Women Finish Rich, and ask each other questions.

Throughout our time together, we'll bring in outside experts including financial advisors, accountants, and personal bankers who will be able to answer any personal financial questions that may come up. Our goal is to create a safe space for you to ask questions and walk away with a full assessment of where you stand financially, along with a plan on how to live out your dreams.

Kelly Green Appointed New Senior Vice President of Farmers State Bank

January 10, 2022 (Harrisburg, Ill.) – Farmers State Bank announced Kelly Green to be new Senior Vice President effective immediately. Green previously held the position of Vice President, Branch Manager, BSA Officer at Southern Illinois Bank.

“We are extremely excited to have a banker with the ability and experience of Kelly Green join our team here at Farmers State Bank,” said Community Bank President Quinn Laird. “She will be an asset not only for the bank, but for the community as well.”

Green brings an exponential amount of banking and leadership experience to her new position. She started in customer service at Herrin Security Bank and eventually worked her way into operations and the position of Senior Vice President. When Green made the move to Southern Illinois Bank, she ended her career there as Vice President, Branch Manager, BSA Officer. Green is a proud Southern Illinois University graduate and has a Bachelor of Science degree in Accounting.

“I am very excited about this new opportunity with Farmers,” said Green. “My main focus is to do what I can for our community and ultimately help individuals and businesses with the financial opportunities to achieve their dreams and meet their goals. I can’t wait for Farmers to be a part of the Herrin Community and I look forward to working with residents there and in the surrounding area. Farmers State Bank is so very special and unique. I believe Herrinites will fall in love with us there and make us their bank of choice.”

Quinn Laird Appointed Farmers State Bank Community President | May 7, 2021

May 7, 2021 (Harrisburg, Ill.) – Farmers State Bank announced its Board of Directors has appointed Quinn Laird as Community Bank President effective immediately. Laird previously held the position of Chief of Police at Herrin Police Department.

“Quinn Laird is an outstanding addition to our team and brings with him a highly respected reputation in our community,” said Charles Holland, CEO of Farmers state Bank. “We are excited for him to join Farmers State Bank.”

Laird brings a strong and diverse set of skills to his new role. He worked in the banking industry as a Loan Officer prior to starting his career in law enforcement. Laird was Sergeant for the Herrin Police Department from July 1997 to June 2015 when he became Chief of Police for the remainder of his career. He retired from law enforcement in August of 2020. Laird is a proud Southern Illinois University graduate and has a Bachelor of Science degree in Finance.

“I’m excited and thankful for this incredible opportunity to work for Farmers State Bank,” said Laird. “I’m really looking forward to being a part of this outstanding organization.”

Farmers State Bank Chairman Can Smell the Roses | April 19, 2021

April 17, 2021 (Harrisburg, Ill.) – Farmers State Bank Chairman of the Board, Tom Franks, can smell the roses! He and son, Ryan Franks, have ownership in a 3-year-old colt named O Besos who was announced as a likely starter in the 147th running of the $3 million Kentucky Derby presented by Woodford Reserve (Grade I) on Saturday, May 1, 2021.

O Besos, a Greg Foley-trained colt, began his career at Churchill Downs. He did his part and officially cracked the lineup of 20 horses for the Run of the Roses as announced in the Kentucky Derby News Update on April 17, 2021. O Besos, who closed for third in the Twinspires.com Louisiana Derby (G2) on March 20, 2021, is not only an improving colt, but also one that will have no problem handling the demanding 10 furlongs of the Kentucky Derby.

“It’s a lifelong dream come true to have a horse running in the Kentucky Derby,” said Franks. “But even in my dreams, I never got this far! It was my father, Bill Franks, lifelong dream as well and he will be going to the Derby with me; I’ll have his picture in my chest pocket. It’s such a blessing. And win, lose or draw, it will be the thrill of a lifetime.”

It’s not every day you can say you have a horse in the Derby and if you’re looking for a hometown hero to cheer this May 1st, O Besos is a solid bet. You can follow along on his road to the Kentucky Derby on the official Kentucky Derby website:

Farmers State Bank Appoints New President and Director of the Board | April 2, 2021

April 2, 2021 (Harrisburg, Ill.) – Farmers State Bank announced its Board of Directors has appointed Brad Henshaw as bank President and member of the Board of Directors effective immediately. Henshaw previously held the position of Community President and Commercial Loan Officer at Farmers State Bank.

“We are fortunate to have someone of Brad Henshaw’s caliber and experience step up to lead Farmers State Bank,” said Charles Holland, CEO of Farmers State Bank. “Brad is one of the founding employees of the bank and has shown exceptional leadership for several years. He has worked extremely hard to help take our bank to another level and I’m excited to have him as President and on the Board of Directors.”

Henshaw brings a wealth of experience to his new role. He started his career in banking at Old National Bank where he was a Loan Review Specialist for a year and a half. Brad joined the Farmers State Bank family on April 1, 1995 as Senior Vice President where he became an expert in Ag and Commercial Lending. With his drive and enthusiasm, he was elected Community President in 2018. Henshaw has a Bachelor of Science degree in Business Administration from Murray State University.

A Guide to COVID-19 Financial Buzzwords | April 20, 2020

Feeling overwhelmed by the inflow of COVID-19 news? FSB created a list of important catchwords circling the internet so you can understand and learn how they may impact you.

Stimulus package

A stimulus package is government-approved and meant to assist the U.S. economy and its residents. In the circumstance of COVID-19, Congress approved the Coronavirus Aid, Relief and Economic Security Act (CARES Act) which uses tax rebates, small business grants, student loan relief and additional funding for healthcare to aid U.S. citizens to stimulate the economy during a time of economic adversity. You’re probably wondering, what does this mean for you? If you’re an individual whose yearly income is under $75,000 (or $150,000 for joint filings), you will receive a stimulus rebate on taxes of $1,200, and an additional $500 per qualifying child. If you make more than $75,000 but less than $99,000 per year, you may still be eligible, though it begins to level out by yearly income. If you’re a small business owner, you may be eligible for a forgivable bridge loan, or additional funding for grants and other specialized assistance.

Furlough

Furlough is a temporary leave some employers can utilize during times of uncertainty, or in the circumstance of COVID-19. A furloughed employee will not be paid during this time but may be asked to return to work when paid staff is temporarily unable. Instead of laying off staff members, employers can put them on furlough, meaning employees can still obtain certain benefits provided by their workplace. (For example, healthcare, dental, etc.) However, during the number of days, weeks, or months these employees are on furlough, they will not be paid by their employer. Although, some furloughed workers may be able to apply for unemployment benefits.

Unemployment benefits or insurance

If you or someone you know has lost a job due to the economic effects of COVID-19, you may be eligible for unemployment benefits. Unemployment benefits are available to those who are unemployed through reasons they weren’t held at fault for, including workers who left their jobs due to COVID-19 regarding their safety and exposure to the virus, those who were laid off because of the economy’s regulations in response to the pandemic, and those who were furloughed. These benefits arrive in government payments that pay a percentage of weekly wages. Keep in mind each state runs its own unemployment benefit program, and percentages and rules differ among them. “To apply for unemployment benefits and get more information, visit your state’s unemployment insurance program website, and soon as many states are experiencing long wait times due to the influx of claims.”

Interest rate

An interest rate is the fraction of an amount loaned which a bank charges as interest to the borrower, normally expressed as an annual percentage. To break it down, when you get a loan, your loan officer will charge you a percentage of your loan amount for borrowing it. Interest rates are fluctuating frequently as the Federal Reserve has lowered them drastically. But what does this mean for you? If you currently have a mortgage with FSB, or even with another bank, it would be smart to consider refinancing while rates are low. If you’re currently on the hunt for a house, it’s also important to lock in a low interest rate to lower your future payments. Speak with a MyFSB Mortgage Lender today, or apply online at: https://www.myfsb.com/loans/home-loans/home-mortgage-loans.html

If you have any further questions, please email [email protected] or call one of our branches at:

Harrisburg: (618) 252-2600

Marion: (618) 998-1188

Alto Pass: (618) 893-2464

Paycheck Protection Program Success | April 10, 2020

Farmers State Bank Successfully Processes Over $30 Million in Small Business Relief Loans, Saves Over 3,955 Southern Illinois Jobs

This past Friday, April 3, 2020, the U.S. Small Business Administration (SBA) rolled out its Paycheck Protection Program (PPP) for small business relief in response to the Coronavirus (COVID-19) pandemic.

But Chris Healy, President of Guaranteed Lending at Farmers State Bank, has been preparing for this moment long before President Trump signed any relief plan into law.

“We saw the need beyond what was currently being offered from the traditional SBA Disaster Programs. Through many phone calls and great relationships formed with individuals in Washington, D.C., we learned about the new program that was underway in the Senate,” said Healy.

“I started reviewing the early versions of the Bill crafted by Senate Republicans well before Leader McConnell introduced it on the floor. We immediately began an informational campaign to let small business owners know help was on the way and shared the early details of the program. While the program went through 312 revisions to become the CARES Act which included the PPP, our customers had a head start in preparing themselves for the application process for funds that would be forgiven,” he added.

Farmers utilized its state-of-the-art electronic application system to intake over 500 applications and collected the required data securely from the applicant well before the PPP went live.

“I believe all of the work that went into this in the weeks leading up to the live rollout was crucial in assisting our communities with securing their funds,” Healy commented.

Not every bank in the market is able to accept applications for the Paycheck Protection Program. Small businesses can only apply through an (existing) approved SBA 7(a) lender, federally insured credit union, or Farm Credit System institution that is participating.

As an approved SBA 7(a) lender, Farmers State Bank is well-known for its guaranteed lending department and was extremely prepared to take on the high volume of loan requests from clients seeking relief in our community and throughout the country.

Friday was the first day those applications could be submitted, which meant Farmers State Bank employees would be putting in a weekend of overtime. The PPP team was comprised of over thirteen lenders, administrators, and processors.These individuals were able to use their specific talents to help retain and restore local jobs and boost our regional economy. These employees worked from 8:00am-11:30pm (or later) Friday through the weekend to put the community’s needs ahead of their own and make a difference.

“From the moment the CARES Act was being discussed we felt a responsibility to our community to stay on top of this disseminate information by all means available and prepared our team to handle the requests of the small businesses to save as many jobs possible,” said Charles Holland, CEO of Farmers State Bank.

In total, the team successfully processed loan applications from over 265 small businesses, amounting to approximately $30 million that will help keep over 3,955 jobs in our region.

“I am so proud of our bank in the undertaking of this monumental task. The team was extremely dedicated in serving small businesses and helped walk them through the process. We were on the phone at all hours, day and night, and our customers were so thankful we were dedicated to work through the weekend to assist them,” Holland remarked.

The Payroll Protection Program is a loan designed to provide a direct incentive for small businesses to keep their workers on the payroll. The SBA will forgive loans under the PPP if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

According to Chris Healy, “These loans are provided to the business owner and cover two months of payroll for employees. It pays employees’ wages, commissions and even tips. There is also an allowance for additional money the small business owner can use to pay rent, utilities and interest expense. The small business owner is not required to provide a personal guarantee and no collateral is required to obtain a loan. When the small business owner uses the funds for payroll, rent, utilities or interest, the loan will be forgiven upon their provision of the receipts to the bank showing those payments.”

In addition to the CARES Act, there are additional loans available directly from the SBA. The Economic Injury Disaster Loan (EIDL) program provides loans of up to $2 million. If approved, these loans allow for the first 12 months of payments to be deferred and are based on a term of 30 years at a rate of 3.75%. A small business can apply for the EIDL as long as there is a different purpose for the usage of funds as compared to that of the PPP loan. A feature of EIDL is an emergency advance for which small business owners are eligible to apply at application. This loan advance will provide up to $10,000 of economic relief to businesses that are currently experiencing temporary difficulties even if they are denied the disaster loan. Your local Small Business Development Center office is a great resource for assistance with applying for the EIDL.

Healy emphasized “The advantage of working with Farmers and other community banks is that we put in the extra work to make sure our customers get the help they need. As many large banks are only allowing their customers to apply for a loan - and won’t accept applications for the first several days due to their technology systems not being fully functional, the local community banks stepped up and got it done! Our community customers had secured funding before the mega banks started taking the available funds from the SBA pool.”

If you have any questions or are interested in applying for a small business relief loan, you can contact the Farmers State Bank guaranteed lending department at [email protected].

Keeping Workers Paid and Employed Act | March 20, 2020

The Keeping Workers Paid and Employed Act would prevent workers from losing their jobs and small businesses from going under due to economic losses caused by the coronavirus pandemic. The plan would provide cash-flow assistance through 100 percent federally guaranteed loans to employers who maintain their payroll during this emergency. If employers maintain their payroll, the loans would be forgiven, which would help workers to remain employed and affected small businesses and our economy to quickly snap-back after the crisis. This proposal would be retroactive to March 1, 2020, to help bring workers who may have already been laid off back onto payrolls.

Small Business Assistance

- Small employers with 500 employees or fewer will be eligible to apply for the loans.

- Loans would be immediately available through existing Small Business Administration-certified lenders, including banks, credit unions, and other financial institutions, and SBA would be required to streamline the process to bring additional lenders into the program.

- The Secretary of Treasury would be authorized to expedite the addition of new lenders and make further enhancements to expedite delivery of capital to small employers.

- The size of the loans would be tied to an applicant’s average monthly payroll; mortgage, rent, and utility payments; and other debt obligations over the previous year. The maximum loan amount would be $10 million.

- Conditional upon business retaining their employees and payroll levels during the covered period (March 1, 2020, through June 30, 2020), the portion of the loan used to cover payroll and payments on pre-existing debt would be forgiven. Further, employers with tipped employees would receive forgiveness for additional wages paid to such employees during the covered time.

- The bill would provide $300 billion to support these loans.

Loan Guaranty Program

- The bill would expand the allowable uses for the existing 7(a) Small Business Administration loan program to permit payroll support, including paid sick leave, supply chain disruptions, employee salaries, mortgage payments, and other debt obligations to provide immediate access to capital for affected small businesses.

- The maximum loan amount for SBA Express loans would be increased from $350,000 to $1 million. These loans provide borrowers with revolving lines of credit for working capital purposes.

- The cost of participation in the 7(a) program would be reduced for both borrowers and lenders by providing fee waivers, an automatic deferment of payments for one year, and no prepayment penalties.

Entrepreneurial Assistance

- The bill would provide grants to offer counseling, training, and related assistance to small businesses affected by COVID-19:

- $240 million for SBA Small Business Development Centers and Women’s Business Centers. The non-federal match for Women’s Business Centers would be waived for a period of three months.

- $10 million for Minority Business Development Agency’s Minority Business Centers

- $25 million for grants to associations representing resource partners.

COVID-19 RELIEF for Small Businesses Act of 2020 | March 20, 2020

SENATE SMALL BUSINESS COMMITTEE DEMOCRATS

American small businesses are facing an unprecedented economic disruption due to the novel coronavirus (COVID-19) outbreak, with reports of small businesses experiencing major difficulties. Due to the nature of this economic disruption, the existing disaster recovery programs for small businesses are insufficient. Congress must find new, innovative ways to help our nation’s small businesses survive the coronavirus outbreak, and build resiliency for the future.

Senate Democrats propose the COVID-19 RELIEF for Small Businesses Act of 2020 to improve and leverage the tools available at the Small Business Administration (SBA) to support small businesses, and create new tools to address the unprecedented pressure that small businesses face, including waiving the disaster declaration requirements so that businesses in all states have immediate access to Economic Injury Disaster Loans.

Further, Senate Democrats support true small business relief through the tax code. These proposals are outside the scope of the Small Business Committee, but we look forward to working with the Finance Committee to ensure tax relief provides the most support possible to the small businesses that need it the most. Details on the proposals for the SBA are below.

Recovery Grants

The federal government has a duty to prevent any small business from falling through the cracks during this public health emergency. For small businesses that are denied an Economic Injury Disaster Loan (EIDL), the bill would create a new grant program to award up to $50,000 to small businesses that meet the following criteria:

- have between two and 50 employees; and

- can demonstrate losses of at least 50 percent for a minimum of one month due to the outbreak.

The grants may be used to address any purpose that would have been allowable under the EIDL program, including:

- providing paid sick leave to employees unable to work due to the direct effect of the coronavirus (COVID–19);

- maintaining payroll to retain employees during business disruptions or substantial slowdowns;

- meeting increased costs to obtain materials unavailable from the applicant’s original source due to interrupted supply chains;

- making rent or mortgage payments; and

- repaying obligations that cannot be met due to revenue losses.

Small Business Debt Relief

Small businesses in industries heavily impacted by coronavirus—such as travel, tourism, and hospitality—are experiencing dramatic cash flow problems. SBA borrowers in the 7(a), 504, and microloan programs are disproportionately in industries likely to be hurt by this crisis. By volume, hotels and restaurants are by far the two largest industries represented. The government is ultimately responsible for guarantees on all of these loans, and has a vested interest in averting mass defaults.

To provide immediate relief to small businesses with SBA-backed loans, the bill would:

- provide small businesses with relief from SBA loan payments, including principal, interest, and fees, for six months;

- encourage banks to provide further relief to small business borrowers by enabling to extend the duration of existing loans beyond existing limits; and

- enable small business lenders to assist more new and existing borrowers by providing a temporary extension on certain reporting requirements.

SBA Major Loan Programs

Unlike large companies, small businesses operate on narrow margins, which makes them more vulnerable to long economic disruptions. Every day, small businesses experiencing disrupted supply chains and mandatory closures for social distancing are losing money—inching toward going out of business.

To get capital to small businesses, the bill temporarily tailors SBA programs to:

- reduce the cost of capital by waiving the fees associated with 7(a) and 504 loans, for borrowers and lenders, for up to 18 months, including for Community Advantage Loans and Export Loans;

- provide a permanent fix to waive fees for veterans and their spouses on 7(a) Express Loans;

- expand the pool of available capital for small businesses by increasing the annual lending limit of the 7(a) loan program, SBA’s long-term loan program, from $30 billion to $80 billion for two years;

- raise the max loan amounts for 7(a) and 504 loans from $5 million to $10 million;

- incentivize lenders to make loans by increasing the guarantee up to 90% on 7(a) loans;

- enhance the 504 refinance program to reach more small businesses who need to refinance expensive fixed assets and lower their payments; and

- boost the microloan program with an additional $72 million in loans, increase how much each lender can loan from $6 million to $10 million, and give borrowers an extra two years to repay.

Direct Lending Program

In addition to leveraging existing SBA programs and the thousands of lending partners that deploy capital to small businesses, small businesses will need a flexible resource for accessing affordable capital to sustain operations, pay workers forced to stay home from work due to the illness, address supply chain interruptions, and other outbreak-related expenses.

This bill establishes a temporary direct loan program at SBA for small businesses located in a State or Territory with a confirmed or presumed positive case of COVID-19. The Business Stabilization Direct Loan Program would:

- provide small business owners capital to pay off or refinance existing debt, provide employee benefits, pay employee wages and related taxes, and acquire technological and other resources that enable continuity of operation;

- support $100B worth of zero interest, zero fee loans of up to $2.5 million each with 10-year terms and repayment deferred for the first year;

- inject money into the economy quickly by mandating that 20 percent of the proceeds be disbursed within 5 calendar days after approval; and

- forgive up to 50% of the loan after December 31, 2021 if the borrower has retained the same number of employees as when they received the loan.

Federal Contracting

The federal government must grant flexibility to small business federal contractors and expedite the contract award process so affected contractors can begin generating revenue. The bill would:

- extend contract performance time by 30 days to small businesses affected by COVID-19;

- require the Federal government to pay small business contractors and revise the delivery schedules, holding small contractors harmless for being unable to perform under a contract because of COVID-19;

- temporarily remove the requirement for contracting officers to conduct market research so that contracting officers may grant sole-source award contracts for small business programs, including the women-owned, HUBZone and service-disabled veteran-owned small business programs;

- increase total sole-source award contract values to $8 million for services and $10 million for manufacturing;

- exclude SBA’s socioeconomic programs, including the 8(a), women-owned, HUBZone and service-disabled veteran-owned programs toward the Office of Management and Budget’s annual category management goals; and

- have federal agencies promptly pay small business prime contractors and contractors with small business subcontractors within 15 days, notwithstanding any other provision of law or regulation, for the duration of the President invoking the Defense Production Act in response to COVID-19.

Entrepreneurial Development

SBA resource partners, including Small Business Development Centers (SBDCs), Women’s Business Centers (WBCs), and the SCORE program, provide vital mentorship, guidance and expertise to small businesses. These organizations will need to hire more staff to deal with the increasing number of small businesses that need their help to respond to COVID-19. The bill would:

- provide $18.75 million in additional funding to WBCs, roughly $150,000 per center;

- inject an additional $40 million into SBDCs;

- grant an additional $1 million to the SCORE program, which is primarily run by volunteer mentors; and

- direct SBA to create a Made in America list to help secure small business supply chains and promote small business manufacturing in the United States.

Community Advantage Program

We know that, in times of economic downturn or uncertainty, underserved markets often experience an even larger credit crunch.

To increase lending to underserved markets, the bill would:

- codify and make permanent the 7(a) Community Advantage program, which has proven successful at increasing lending to women, minorities and veterans by providing loans of up to $250,000 through mission lenders;

- expand the program’s geographic and demographic reach to cover women and minorities; and

- increase the amount of available capital by allowing the Administrator, at her discretion, to provide waivers for loans to go up to $350,000.

This legislation builds on lessons learned over the past nine years, creating guardrails for responsible growth and increasing oversight to mitigate risk.

Intermediary Lending Program

Responding to the economic impact of this public health crisis requires fast, flexible and targeted deployment of capital to the communities most affected. The bill would reinstate and make permanent the Intermediary Lending Program (ILP), which would give direct loans of up to $1.5 million to nonprofit lenders, who then lend to small businesses in their communities with loans of up to $200,000.

The program would:

- leverage the on-the-ground knowledge of nonprofit lenders to get capital to the communities and small businesses that need them most;

- increase the amount of capital available for small businesses in the most affected communities; and

- help manufacturing and high tech firms ramp up production by deferring principal and interest payments for up to 6 months.

Small Business Resiliency

After small businesses make it through this difficult period, the federal government must do all it can to ensure that they are more resilient and better prepared for the next economic disruption, whether it’s a natural disaster or a cyberattack on their business. The bill would:

- allow small businesses already approved for an EIDL to borrow an additional 20 percent beyond what they have been approved for to pay for business continuity and resilience improvements, including establishing telework capability and implementing off site record keeping, among other measures.

The provision is similar to rules in SBA’s physical disaster loan program that allow businesses to take out an additional 20 percent to pay for hazard mitigation to better withstand the next natural disaster.

Office of Emerging Markets

After the Great Recession, SBA created an office to bring “greater unity, focus and effectiveness to SBA’s efforts” to reignite economic opportunity for underserved, or emerging, markets. The office was unique, did great work, and was considered vital by stakeholders, however it is now vacant.

It is vital that the additional resources and tools provided to SBA be deployed in a strategic manner to ensure that SBA-backed capital is directed to the communities that struggle the most to access capital in the private markets.

The bill would create the Office of Emerging Markets within SBA to:

- create and implement strategies and programs that provide an integrated approach to the development of small business concerns in emerging markets;

- develop and recommend policies concerning the microloan program and any other access to capital program of the Administration;

- establish partnerships with those best positioned to advance the goal of improving the economic success of small business concerns in an emerging market; and

- review the efficacy and impact of the microloan program and any other access to capital program of the Administration, as it pertains to emerging markets.

Innovation Centers Program

Underserved communities have been left out of many of the economic gains that have occurred since the Great Recession. Many of these communities are now expected to be among the hardest hit by COVID-19. As our economy recovers from this pandemic, we must ensure that these communities are not left even further behind.

The bill would create the Innovation Centers Program within SBA to:

- support the creation and retention of dignified work that offers good salaries and pathways to prosperity;

- prioritize inclusivity in innovation to ensure that groups currently underrepresented in high-growth industries get the support they need to be successful;

- establish new entrepreneurship ecosystems by using HBCUs, MSIs, and community colleges, which are critical to reaching minority, low-income, and rural populations, to foster entrepreneurship in their communities; and

- enhance outcomes for underserved business owners by creating projects that will combine unique and intensive mentorship, networking, and sometimes funding opportunities to fill a gap in SBA’s current programming.

Small Business Innovation Research & Small Technology Transfer Research Programs

The Small Business Innovation Research Program and the Small Technology Transfer Research Program allow government agencies to partner with high-tech small businesses to conduct vital government research in areas, such as renewable energy, cybersecurity and biosciences.

The bill would make the programs permanent, providing certainty that roughly $3.5 billion in seed capital continues to flow into local our communities annually, require civilian agencies to accelerate the timelines for awards to as close to 90 days as possible so small businesses are able to act quickly.

Trade

The State Trade Expansion Program (STEP) awards funds to be used to increase small business exporters and their sales in their state. Entities who have been awarded funds under the program in fiscal years 2018 or 2019 will struggle to use all of those funds before the deadline due to the impacts of COVID-19 on international trade and exports. Currently, unobligated funds cannot be carried over into the next fiscal year.

This bill would support small business trade and exporting by allowing states to carry over STEP funds from FY18 and FY19 into FY21 to ensure that they still have access to that money once normal business resumes.

Government Small Business Relief | March 18, 2020

To keep you informed is our priority in these times of great uncertainty. The government is working on a 3 Phase approach to combat the economic downturn directly related to the Coronavirus (COVID-19).

Phase 1

Phase 1 is approved and funded via the SBA Economic Injury and Disaster Loans and are available in many states with more states coming on line each day. A breakdown of that program is as follows:

SBA’s Economic Injury Disaster Loans offer up to $2 million in assistance for a small business. These loans can provide vital economic support to small businesses to help overcome the temporary loss of revenue they are experiencing.

Process for Accessing SBA’s Coronavirus (COVID-19) Disaster Relief Lending

- The U.S. Small Business Administration is offering designated states and territories low-interest federal disaster loans for working capital to small businesses suffering substantial economic injury as a result of the Coronavirus (COVID-19). Upon a request received from a state’s or territory’s Governor, SBA will issue under its own authority, as provided by the Coronavirus Preparedness and Response Supplemental Appropriations Act that was recently signed by the President, an Economic Injury Disaster Loan declaration.

- Any such Economic Injury Disaster Loan assistance declaration issued by the SBA makes loans available to small businesses and private, non-profit organizations in designated areas of a state or territory to help alleviate economic injury caused by the Coronavirus (COVID-19).

- SBA’s Office of Disaster Assistance will coordinate with the state’s or territory’s Governor to submit the request for Economic Injury Disaster Loan assistance.

- Once a declaration is made for designated areas within a state, the information on the application process for Economic Injury Disaster Loan assistance will be made available to all affected communities.

- These loans may be used to pay fixed debts, payroll, accounts payable and other bills that can’t be paid because of the disaster’s impact. The interest rate is 3.75% for small businesses without credit available elsewhere; businesses with credit available elsewhere are not eligible. The interest rate for non-profits is 2.75%.

- SBA offers loans with long-term repayments in order to keep payments affordable, up to a maximum of 30 years. Terms are determined on a case-by-case basis, based upon each borrower’s ability to repay.

- SBA’s Economic Injury Disaster Loans are just one piece of the expanded focus of the federal government’s coordinated response, and the SBA is strongly committed to providing the most effective and customer-focused response possible.

For additional information, please contact the SBA disaster assistance customer service center. Call 1-800-659-2955 (TTY: 1-800-877-8339) or e-mail [email protected](link sends e-mail)

Phase 2:

The U.S. House and Senate have approved Phase 2 stimulus to combat the economic toll put on our small business owners and employees. That has currently been sent to the President for his signing into law that seeks to help those that are sick from being able to work or forced to stay at home to care for loved ones due to illness or closures from the Coronavirus.

All eyes are now locked onto Phase 3 of stimulus that is set to be much more widespread and massive. The following is an outline of what is trying to be accomplished.

Phase 3 Proposal:

- APPROPRIATION TO THE EXCHANGE STABILIZATION FUND FOR SPECIFIED USES

-

- Airline Industry Secured Lending Facility ($50 billion)

- This provision would appropriate an additional $50 billion to the ESF and authorize use of those funds for secured lending to U.S. passenger and cargo air carriers

- Treasury Department to determine appropriate interest rate and other terms and conditions

- Secured by collateral specified by the Treasury Department

- Requirements on borrowers would include:

- Specified continuation of service requirements

- Limits on increases in executive compensation until repayment of the loans

- Airline Industry Secured Lending Facility ($50 billion)

-

- Other Severely Distressed Sectors of the U.S. Economy ($150 billion)

- This provision would appropriate an additional $150 billion and authorize use of those funds for secured lending or loan guarantees to assist other critical sectors of theU.S. economy experiencing severe financial distress due to the COVID-19 outbreak.

- Other Severely Distressed Sectors of the U.S. Economy ($150 billion)

- TEMPORARILY PERMIT USE OF THE EXCHANGE STABILIZATION FUND TO GUARANTEE MONEY MARKET MUTUAL FUNDS

- Temporarily suspend the statutory limitation on the use of the Exchange Stabilization Fund (Section 131 of the Emergency Economic Stabilization Act of 2008) for guarantee programs for the United States money market mutual fund industry.

- Sunset date: Terminate authority to establish any new MMMF guarantee program upon the conclusion of the National Emergency Concerning the Coronavirus Disease 2019 (COVID-19) Outbreak declared by the President on March 13, 2020.

- ECONOMIC IMPACT PAYMENTS

- This provision would authorize and appropriate funds for two rounds of direct payments to individual taxpayers, to be administered by the IRS and Bureau of the Fiscal Service.

- $250 billion to be issued beginning April 6

- $250 billion to be issued beginning May 18

- Payment amounts would be fixed and tiered based on income level and family size. Treasury is modeling specific options.

- Each round of payments would be identical in amount.

- This provision would authorize and appropriate funds for two rounds of direct payments to individual taxpayers, to be administered by the IRS and Bureau of the Fiscal Service.

- SMALL BUSINESS INTERRUPTION LOANS

-

- To provide continuity of employment through business interruptions, this provision would authorize the creation of a small business interruption loan program and appropriate $300 billion for the program.

- The U.S. government would provide a 100% guarantee on any qualifying small business interruption loan.

- Qualifying loan terms:

- Eligible borrowers: Employers with 500 employees or less (phased out)

- Loan amounts: 100% of 6 weeks of payroll, capped at $1540 per week per employee (approx. $80,000 annualized)

- Borrower requirement: Employee compensation must be sustained for all employees for 8 weeks from the date the loan is disbursed.

- Lender: U.S. financial institutions

- Streamlined underwriting process: Lender verifies the previous 6-week payroll amount and later verifies that the borrower has paid 8 weeks of payroll from date of disbursement.

- Authority for the Treasury Department to issue regulations establishing appropriate interest rate, loan maturity, and other relevant terms and conditions

We anticipate that the SBA will continue to play a huge role in this plan. As a Preferred SBA Lender, Farmers State Bank is eagerly waiting on these new tools and we will expedite funds to immediately help this nations small business owners. Many of you have already been reaching out. Please do not hesitate to call Chris Healy at (812)589-2018 or email [email protected] to discuss your current needs.

D. Matthew Businaro Appointed New CFO of Farmers State Bank | June 6, 2018

June 6, 2018 (Harrisburg, Ill.) – Farmers State Bank is proud to announce the appointment of David Matthew Businaro, CPA, as their new Chief Financial Officer effective May 1, 2018. As CFO, his responsibilities will include the management of financial reporting, budgeting, internal audit, corporate governance, accounts payable, capital planning and investments.

Businaro graduated from Southern Illinois University in Carbondale, IL with a degree in accounting. He joined Farmers State Bank most recently from Kemper CPA Group where he was employed since 2000 and admitted partner in 2007. His main responsibilities were centered on income tax compliance and consulting and auditing financial statements of small governments, nonprofit organizations, and small businesses.

“Matthew brings significant experience in accounting operations and strategic planning to Farmers State Bank, and we are thrilled to have him on our team,” said Charles Holland, CEO of Farmers State Bank. “His expertise will be extremely beneficial in managing our finances, increasing our lending capacity, and continuing our trajectory of success. Our mission is to provide strong community banking for our southern Illinois communities and we are confident Businaro will be an invaluable asset in fulfilling this mission.”

Farmers State Bank Strengthens Mortgage Division | September 18, 2017

September 18, 2017 (Harrisburg, Ill.) – Farmers State Bank is reinforcing its position as number one in mortgage banking in southern Illinois with the appointment of John Streuter who joined the organization on August 28th, 2017.

John Streuter assumes the role of Executive Vice President and Chief Mortgage Officer. In this position, Streuter will manage a team of loan officers, mortgage originators, and loan processors that specialize in working with individuals to purchase or refinance homes. Streuter has more than 32 years of experience as a mortgage banking producer and manager. He attended SIU Carbondale, ILSI School of Banking, and has completed multiple seminars on consumer lending, real estate lending, appraisals and underwriting.

"I’m beyond excited to have John Streuter join our family as the leader of our mortgage department," said Tom Franks, chairman of the board. "John brings years of leadership, experience, and true professionalism. I’m convinced he’s the top mortgage guy in the tri-state area."

FSB Appointments New Bank President | September 6, 2017

September 6, 2017 (Harrisburg, Ill.) – Farmers State Bank is honored to announce the appointment of Steven W. Cook as the new President of the bank, effective August 15, 2017. Cook takes the helm as President of the bank with the appointment of Charles M. Holland as the new CEO. Cook currently serves the company as Community Bank President in Marion, IL and has served in that capacity for the last twelve years. With strong and seasoned leadership in place, Farmers State Bank is positioned to exponentially build on its current growth and success.

“I’m excited to have Steve’s leadership at the reins of Farmers State Bank,” said Tom Franks, Chairman of the Board. “He brings years of integrity and community banking experience. I personally think Steve Cook is the best community banker in America.”

Cook earned a bachelor’s degree in business from Southern Illinois University in Carbondale, and he later completed the Graduate School of Banking at Louisiana State University in 2000. He began his career as a bank examiner with the State of Illinois Commissioner of Banks and Trust Companies. Later, Cook was a successful producer in the securities industry where he held his investment license and full line insurance producer licenses. In 1995 Steven accepted a position with Citizens Bank, now Fifth Third Bank, in Harrisburg, IL, as a commercial lender. He held various roles in multiple markets within the organization including Senior Lender, Regional Manager, and City Executive over the 10 years with the company and was recognized as a leading producer for the company. Cook joined Farmers State Bank as Community Bank President in 2005 and has played a major role in the company’s growth over his tenure here at Farmers. With over 28 years of industry experience and in-depth knowledge, Steven is a team-oriented leader with the skills, experience, and commitment to take on the responsibilities of President.

Charles M. Holland Appointed New CEO | August 29, 2017

August 29, 2017 (Harrisburg, Ill.) – Farmers State Bank is proud to announce the appointment of Charles M. Holland as their new Chief Executive Officer. Holland, who currently serves as Farmers State Bank’s President will succeed Greg Taake, current CEO effective August 15th, 2017.

Charles, 38, earned a bachelor’s degree in accounting from Southern Illinois University in Carbondale. He joined Farmers State Bank in 2002 and has since held various positions within the organization. Holland has a record of strong leadership both inside and outside of the banking world. This, combined with his deep industry knowledge and institutional tenure, makes Charles uniquely qualified to lead Farmers State Bank successfully into the future.

"I have complete confidence in our new CEO, Charles Holland," said Tom Franks, Chairman of the Board. "There is no doubt he has the vision and leadership to take us from a good to great bank. I’m extremely excited for the future of Farmers State Bank with him in control and look forward to providing a higher level of excellence in service for all communities in Southern Illinois."

{endAccordion}